At first glance, DeFi looks weak right now.

Prices are volatile, total value locked has dropped from recent highs, and capital is clearly rotating back into Bitcoin. The headlines focus on fear, outflows, and geopolitical risk and right now, those headlines aren’t wrong. We covered exactly how that macro pressure is affecting crypto markets following the March 26 selloff.

But that surface-level view misses what’s actually happening underneath.

Because structurally, DeFi isn’t collapsing. It’s evolving, and the data behind that evolution is striking.

The Surface: Volatility and Capital Rotation

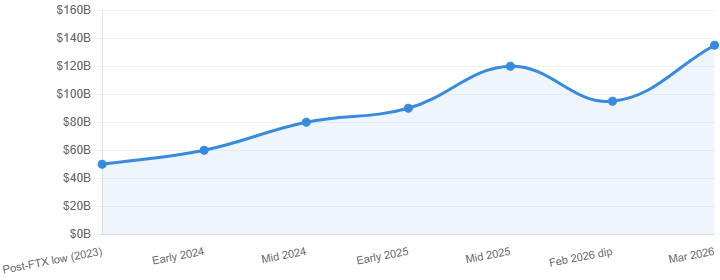

Total DeFi TVL across all chains sits around $130–$140 billion in early 2026, up from a post-FTX low near $50 billion but still below peak bull-market levels. That number dropped sharply in February, briefly falling below $100 billion before recovering.

At the same time, Bitcoin dominance has climbed above 56%, showing a clear shift in how capital is being positioned. This isn’t random. It’s defensive behavior. In uncertain markets, especially with oil above $100 and the Iran conflict ongoing, investors move away from high-risk assets toward what they perceive as safer ones. In crypto, that means Bitcoin. And DeFi tokens, especially smaller ones, sit at the opposite end of that risk spectrum.

The chart above illustrates the broader trajectory: despite the February dip, DeFi TVL has tripled since the post-FTX bottom. The current pullback is real but it exists within a longer-term recovery. You can track live TVL data at any time on DefiLlama.

What’s Actually Changing: Fundamentals Over Narrative

This is where the real shift is happening.

In previous cycles, DeFi moved as a single narrative. Everything went up together regardless of quality — governance tokens, yield farms, speculative protocols, all riding the same wave. That’s no longer the case. Performance is now fragmented and selective.

Leading blue-chip protocols include Lido with about $27.5 billion in TVL, Aave with $27 billion, EigenLayer with $13 billion, Uniswap with $6.8 billion, and Maker with $5.2 billion. These are protocols that generate real, measurable revenue, through fees, lending spreads, and trading activity. Meanwhile, purely speculative or governance-heavy tokens are underperforming.

That’s a sign of maturity. The market is starting to price DeFi not as a single story, but as a set of individual businesses some of which are now genuinely profitable.

The Rise of Institutional DeFi

It’s no longer just retail traders chasing yield.

Institutional capital is entering DeFi, but in a very different way than the retail waves of 2020 and 2021. Instead of speculation, institutions are using DeFi as a kind of on-chain fixed income system: earning yield through lending, using tokenized assets like Treasuries, and reducing operational costs compared to traditional finance.

At Consensus Hong Kong 2026, leaders from Animoca Brands, Mastercard, and Robinhood highlighted that the focus is on tokenized U.S. Treasuries, money market funds, stablecoin integrations, and better ways to manage collateral. BlackRock COO Rob Goldstein called blockchain “the biggest financial breakthrough since double-entry bookkeeping.”

This changes the entire dynamic. DeFi is slowly becoming infrastructure, not just a trading playground.

Real-World Assets (RWA): The Biggest Structural Shift in DeFi Right Now

If there’s one trend defining DeFi in 2026, it’s the movement of real-world assets onto the blockchain.

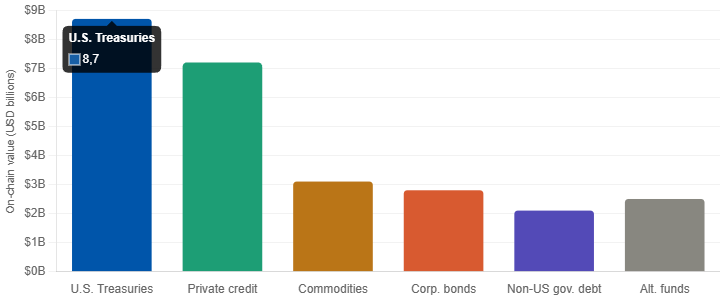

The value of tokenized real-world assets has increased nearly fourfold in the last year, surpassing $26.4 billion in on-chain value, up from around $6.6 billion a year ago, according to RWA.xyz. Six categories of tokenized assets have passed the $1 billion mark: private credit, commodities, U.S. Treasuries, corporate bonds, non-U.S. government debt, and institutional alternative funds.

Major financial institutions such as BlackRock, Franklin Templeton, and JPMorgan have already launched tokenized funds. According to rwa.xyz, there’s about $8.7 billion in on-chain U.S. Treasuries, still only a tiny fraction of the almost $28 trillion in issued U.S. Treasuries, leaving enormous room for growth.

According to Ivo Grigorov, CEO of Real Finance, RWAs will move from “tokenized experiments to repeatable, standardized on-chain financial products” in 2026, driven by $130 trillion in outstanding fixed-income markets and persistent inefficiencies in traditional finance.

This is important because it connects DeFi to something it didn’t have before: real, external cash flows that don’t depend on crypto market cycles. RWAs provide yield and collateral that exists regardless of whether Bitcoin is up or down. For a deeper dive into how this fits into the broader crypto regulatory picture, see our article on what MiCA means for digital assets in Europe.

Where the Activity Is Moving: Chains and Products

Ethereum still dominates DeFi infrastructure, commanding about 68% of all DeFi TVL and remaining the primary hub for institutional activity. Solana has emerged as a clear secondary hub with about $9.2 billion in DeFi TVL, rivaling the combined major Ethereum Layer 2s.

But the most striking shift isn’t happening in which chain is winning. It’s in which product is exploding.

Perpetual DEXs: DeFi’s Fastest-Growing Sector

Decentralized derivatives have gone from a niche product to a dominant force in a remarkably short time.

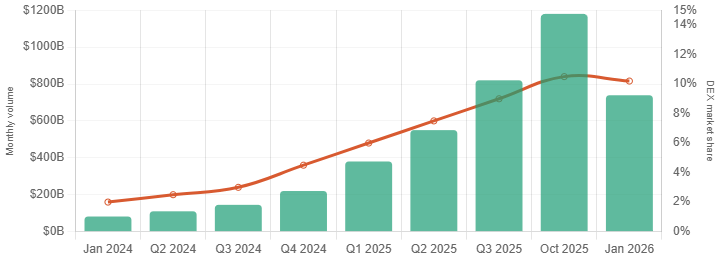

Total perpetuals trading volume grew 75% from $4.14 trillion in January 2024 to $7.24 trillion in January 2026, with some months exceeding $10 trillion. Monthly perpetual DEX volume grew nearly eightfold over the past two years, from $81.7 billion to $739.5 billion, with DEX market share rising from just 2% to over 10%. The Motley Fool

Hyperliquid dominates the perp DEX landscape, holding roughly $9.57 billion in open interest more than all other major perp DEXs combined. Weekly trading volume regularly exceeds $40 billion, representing approximately 32% of all decentralized perpetual trading. Yahoo Finance

What’s particularly notable is that this growth is happening during a bear market for most crypto prices. Since early 2025, DEX market share has remained consistently above 10%, suggesting that on-chain trading is no longer purely cyclical. And the Iran shock is accelerating it: when oil futures trading on Hyperliquid reached $7.3 billion on March 13, precisely while traditional markets were closed, it highlighted how decentralized and always-active platforms are becoming essential tools for price discovery in situations of global volatility.

Traditional markets close at 5pm. DeFi never does.

Regulation Is Quietly Reshaping DeFi

This is another major shift that most people underestimate.

The industry is splitting into two clear paths:

- Compliant DeFi — built for institutions, with identity layers, KYC, and regulatory alignment

- Pure DeFi — fully decentralized, operating outside traditional regulatory frameworks

In Europe, MiCA is already forcing changes. Our full breakdown of the MiCA Act explains how it works in detail, but the key point for DeFi is this: MiCA draws a clear line between protocols with identifiable intermediaries (regulated) and genuinely decentralized protocols (excluded). That line is now being enforced, with the final deadline for all firms to hold a MiCA licence arriving on July 1, 2026.

In the U.S., 2026 marks the passage of major global legislation including the U.S. Genius and Clarity Acts, which have solidified crypto as a standard institutional asset class. Clearer asset classification reduces uncertainty, and uncertainty was one of the biggest reasons institutional capital stayed on the sidelines for so long.

The result is a more structured environment. That creates higher barriers, but it also makes DeFi genuinely usable for major institutions for the first time.

The Risk Side: Still Very Real

Even with these improvements, DeFi remains volatile and carries risks that don’t exist in traditional markets.

We’ve seen examples this cycle where individual protocols dropped over 50% in days, not because the technology failed, but because of market structure, liquidity conditions, or governance failures. The macro environment we described in our stock market crash analysis makes this worse: when fear spikes and liquidity contracts, DeFi reacts faster than the broader crypto market.

New structural risks are also emerging in 2026:

Geofencing. Platforms are increasingly blocking users in certain jurisdictions due to regulatory pressure, fragmenting access and liquidity.

Oracle risk. For RWAs used as collateral in DeFi, if an oracle reports an incorrect price for a tokenized asset, it could trigger improper liquidations or allow undercollateralized borrowing. Most RWA protocols use a combination of Chainlink price feeds and manual attestations, but the oracle layer remains a single point of failure in many integrations.

Regulatory fragmentation. A tokenized asset that is legal to hold in Singapore may not be accessible to U.S. investors, and transfer restrictions encoded in smart contracts may not align with the laws of every jurisdiction where token holders reside. Cross-border enforcement of token holder rights remains largely untested in courts.

None of these risks are fatal to the sector. But they are real, and they matter for anyone deploying capital into DeFi right now.

DeFi’s Trajectory: The Numbers That Matter

Here’s a snapshot of where DeFi stands in March 2026, by the numbers:

The overall DeFi market size is about $238.5 billion in 2026, projected to reach $770.6 billion by 2031 on a 26.4% compound annual growth rate. That trajectory is being driven not by speculation, but by real institutional adoption, RWA growth, and the structural shift toward on-chain derivatives.

So What Does This All Mean?

DeFi in 2026 is in a transition phase and that’s precisely why it looks quiet on the surface.

On the surface: prices are unstable, capital is rotating out, and sentiment is cautious. But underneath: infrastructure is maturing, institutional capital is entering with clear purpose, real-world assets are connecting DeFi to $130 trillion in traditional financial markets, and decentralized derivatives have become a serious competitor to centralised exchanges.

As Artem Tolkachev, chief RWA officer at Falcon Finance put it: “The next phase is about collateral usability. Institutions don’t just want tokenized assets sitting in isolation.” They want those assets working, generating yield, acting as collateral, plugging into lending and derivatives markets.

That’s exactly what DeFi is building right now.

This combination of improving fundamentals paired with depressed prices and cautious sentiment, doesn’t usually produce immediate upside. But historically, it does produce the structural foundations for the next major cycle. And right now, those foundations are getting measurably stronger, even if price action doesn’t show it yet.

1 Comment

Pingback: Crypto Weekly: The $14B Options Expiry, Geopolitical Shock, and Market Reset (March 23–27, 2026) – Dailycoinradar